Would you like to know why car payments suck? New numbers were recently released showing the average purchase price for a new car went up to an all-time high of $32,352. No one has liquid cash available to shell out $32k on a car, so the numbers also show the amount borrowed on new cars hit an all-time high of $28,381. In the end, borrowers are dragging around a $482/month payment at 4.5% for 67 months – a new all time record! Super.

At the same time, 70 percent of Americans are living paycheck-to-paycheck. People are barely scraping by and they can’t remember the last time they actually had a little fun with their money. I get letters all the time asking what I would do if I were in their shoes. The majority of the time, it’s simple: Get rid of your car (payment).

We may not realize our cars are killing our financial plan, but I am here to tell you this:

Car Payments Suck.

Period.

Car Payments are Not a Way of Life

We often believe they are because of how we are trained to think about car payments. We are taught to simply ask “How much down and how much a month?”

Poor people ask “How much down and how much per month?” Rich people simply ask “How Much?”

With that said, let’s look at some FUN FACTS about car payments:

With that said, let’s look at some FUN FACTS about car payments:

• Average Car Payment in 2015: $482/ month over 67 months at 4.5% interest

• Average Price of New Car Financed in 2015: $32,352

• Value of car 48 months later: $12,800

• Amount owed on car 48 months later: $8,850

Over the next 48 months, you would have paid $23,136 for the car and you still have 18 more months of payments. This is also right around the time where our love for cars creates car fever and we end up needing a new car because the “Check Engine” light came on. We start believing car payments are just part of life.

Poor me. Whah, whah, whah. I guess I’ll just never get ahead. Whah whah whah.

Have an Auto Loan with a High Interest Rate?

You could try getting a lower rate to pay that thing down faster

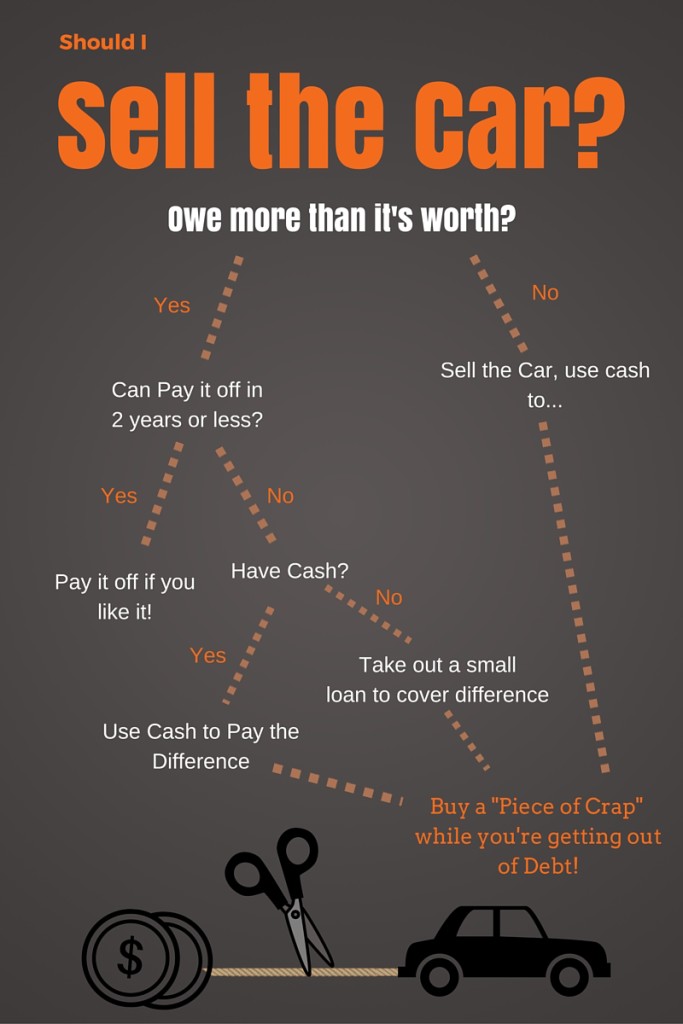

Upside Down in Car Payments?

Download the Entire Step-by-Step Guide to Getting Out From Underneath Your Upside Down Car

Upside Down Car Guide

Start Thinking Differently

It’s time to choose a new direction with your money. The truth is car payments don’t have to be a way of life. I am here to tell you that this belief is simply garbage and you don’t have to put up with it anymore! I tell this to people all the time during our seminars and one-on-one coaching sessions. And, guess what? It’s beginning to catch on 🙂

Here are some real-life stories of those who finally decided to take a stand against car payments and completely change the trajectory of their financial lives. This is what I often refer to as Awesome.

Meet the People who Kicked their Payments to the Curb

Jeff and Jillian pay off 3 vehicles and add $10k/year to their Budget

Jeff and Jillian pay off 3 vehicles and add $10k/year to their Budget

They saved $860/month when they paid off 3 vehicles. They are now on their way towards debt freedom much faster because they no longer have $10k/year going out in the form of payments. Hello!

We went from 3 car loan payments to ZERO in 7 months. No car payments= more cash flow ?. More cash flow=better quality of life! Thanks for all your financial guidance Chris Peach!

Esteban and Stacy add a Paid For Car and $388 into the Monthly Budget

Esteban and Stacy add a Paid For Car and $388 into the Monthly Budget

You know what they call a car after you make your last payment on it? Yours. Every night when they park the car in the garage, they know it is all theirs and no one can come take it from them. They own it. Oh yeah, they also just got a $4,600/year raise!

We want to thank you for all the great financial advice. The Garzas read and love your blog. Since we have come across your blog, we have implemented a budget that works great for our needs today, tomorrow and our future. We paid off this car in August and are proud to say we are debt free. Also, we have a sinking fund!!! That fund is fun!!! Once again, thank you for your wonderful blog!!!

Pam and Gunnar Get the Title to her Car and add $315/month towards their Debt Snowball

Pam and Gunnar Get the Title to her Car and add $315/month towards their Debt Snowball

When I met with Pam and her husband, she had no idea how close she was to paying off her car. Sometimes when car payments are just a way of life, you almost forget that they can one day go away. She sent off her last payment and now she is the OWNER of a 2006 Mitsubishi Endeavor and the recipient of an extra $315 each month to throw at her Debt Snowball. Insert Virtual Fist Bump Here.

Thank you Money Peach for guiding us through our plan of attack for paying off debt! You truly made what I thought was going to be horrific and painful actually turned into feeling like a 10 ton weight lifted off! One of the greates eye openers was seeing that I could pay off my car within the first month! Talk about a catapult into getting this party started!! Your enthusiasm and love for empowering others with their finances is second to none!

Jason goes from a $21k Truck Loan to a nice Paid For Car in 10 Months

Jason owed $21k and four more years of $500/month payments on his Toyota Tundra. Luckily he was able to sell his truck for just about what he owed on it and paid off his loan on his Tundra. He found a used Chrysler 300 for $4,500 and took out a smaller loan to buy it. His new payment is now $110/month, however he continues to make the $500/month payment he was used to. By selling his truck and buying a used car, he will have gone from four years of truck payments to a paid off car in about 10 months. Not too shabby!

Ansel and Sheryl wipe out $32k and save $1,100 every month

They sold his truck and wiped out $32k in Debt in one transaction. Then they did the unthinkable: They purchased a 2004 Lincoln and created an extra $1,100 in their Budget each month! Basically, their family just created an extra $13k every year to throw at debt and they are driving a car that isn’t dropping in value like a rock! Yes, the black truck is going to impress more people at the next stop light than the Lincoln. However, apparently Ansel would rather save $1,100 a month than impress a stranger for 7 seconds at the next traffic light. Choices can be fun….

Are You Next?

If these people can go from ordinary to awesome, why can’t you? What gets in the way is our behavior. Some of us even have this in our minds:

“How will I possibly get out of bed without the car I am driving now?”

You get to make the choice to get out of debt, stay out of debt, and build wealth. Think about that – you get to choose. If you are ready, the best time to get started is right now. Cut away the car payment that is dragging your life down and free yourself from the chains of debt. Forever.

If You Like it, Please Share it!

As always, I first want to thank you for reading this blog because this means you are reaching for awesome with your money! I will keep putting content out there for anyone to gobble up and implement right away, however if you could help me out by sharing this post on your favorite social media platforms, it would mean the world to me! Just click on any of the social share buttons at the top or bottom of this post and you’ll be giving me a virtual fist bump, high-five, and a pat on the back. Thank you again and again!

-Chris Peach

55 Comments

A lot of folks have this monthly mindset and it’s extremely dangerous because you end up overpaying for so much. It’s really just the reverse of deferred gratification. When you get the product first but actually for it later, you pay way more for it.

The crazy thing is that $500 a month on minimum wage is ~63 hours, that’s before you deduct taxes. A car isn’t that valuable. It’s not worth 63 hours.

Hi Jim,

I never even thought of it in terms of using the minimum wage scenario as compared to the monthly car payment. Great point. I interviewed a couple who made an above average family income in May because they literally had a car payment that was more thant their house payment. Needless to say, those days are in their past, but there was a time where they accepted the fact their car payment was more than their house payment. This shocks so many when they hear about it, however it’s not as uncommon as one may think. These stories also keep financial bloggers typing away at their laptops too! Thanks for the comment Jim!

I hate car payments! One thing that I always try to think about is how many hours I’d have to work in order to pay a car payment. Granted, it’s significantly less hours now than it used to be, but I’m still not willing to send all the money I worked for toward a car payment.

Hi Cat!

Not only are you not willing to send your hard earned money over in the form of car payments, but the payments are also going towards something that is dropping value like a rock! Consumer Reports and some 5th grade math will tell you brand new cars lose 60% of their value in the first 4 years. No thank-you! Rule of thumb: If you can pay the car off in 2 years or less and you like the car, keep it. If not, sell off your car and your car payment! It may be killing your financial plan – not yours Cat 🙂 Thanks for the comment!

True post about “How can I get out of bed if I don’t have this car.” I spoiled myself and bought a preowned 2012 Mustang GT (paid off), my dream car for a single person. Add a wife & 4 month old baby & soon needing to get a more reliable replacement family vehicle and you get in the pickle seeing how much that “new” car has devalued in several years. Still has enough value to where we can sell it, buy a cheaper vehicle, and pocket the difference. But makes you sick knowing in 4 years time a vehicle has devalued $15,000 from the original sticker price ($7k from what I purchased).

Josh,

I cannot agree with you more. You are wise because you are looking at the Opportunity Cost of Driving any car. Once we started realizing that cars were merely a depreciating piece of metal, we started buying older cars to avoid the opportunity cost of missing out on investing our money in things that go up in value. This is why we choose to drive pieces of crap 🙂 Thanks for the comment Josh!

Thanks for the link. Definitely resonates with our thought process. Something with some mileage but still dependable for that 8-12 hour car trip as we make the annual pilgrimage to my family multiple zip codes away.

We have been using your budget spreadsheets and reading your blog since July and just paid off our 2008 Chevy Tahoe! We sold my husband’s Denali and paid cash for a small commuter car! No more car payments! We now have $375 extra to throw towards our debt snowball each month. Since July we have paid off over $25,000. Thank you for all of your great advice!

Hi Carrie!

So you are saying you paid off $25k since July and created $375 each month to throw at debt? Wow! I am beyond impressed. You guys are rocking it and don’t stop. I would love to hear more about your success. Look for an email from me soon! Congrats to you both – very impressive 🙂

Hi, I clicked over from Club Thrifty’s Facebook link. Nice place you’ve got here. 🙂

About 6 months after I paid off my used, 10-year-old Volvo wagon (I think “Volvo” is Swedish for “money pit”), it had YET MORE problems and my mechanic talked me into getting rid of it, which I did (sold it to a dealer for $600). Fortunately, I had had the foresight to bank the payments I’d been making ($250/month) to cover ongoing repairs and, since my guy basically refused to fix it anymore, I had just enough in the account to buy a (very) used minivan (which, as it turns out, is far more practical, if not more comfortable, than the Volvo was). No payments, no collision insurance – just money going into the bank.

Almost exactly a year later, I was rear-ended on the way to work and the van was totaled. Although the other insurance company would reimburse me (eventually) I was fortunate enough to have enough in the bank to find an almost identical minivan, walk into the dealer, and write them a check. It was another 2 months before I received that reimbursement check.

So yeah, car payments suck. And the lack of car payments = freedom. 🙂

Hi Kris! I love Club Thrifty so I’m glad they sent you over. Your story is a perfect example of how it works when implemented perfectly. You paid off your old car and then instead of going out and spending like “cray cray”, you saved the money for a rainy day – or when someone totals your mini van. I love your story! Thanks for sharing and I looked it up – Volvo means “we take your money now and forever” 🙂

I too had a money pit Volvo that I finally sold. A friend had a used car for sale for under value with an extended warranty that transferred. I miss not having a car payment but don’t miss all the breakdowns and repair costs. We are throwing money at the payments and should have the newer car paid off by the end of the year for a vehicle that should last me at least 10 more years!

New cars suck, car payments suck, you’re brand new hybrid sucks….bottom line….depreciation sucks! And paying interest on a depreciating asset is the same as using $100 bills as fire starter to burn 1 iPhone a month! It’s insanity!

Love your flow chart. I made one once. But it asked “Do I Need a New Car”, and no matter which path you followed, the answer was “NO!”

Nice work, Peach. Killer post here. Sharing now!

Thanks Jacob! I would love to record you saying the first sentence above – that would be a killer commercial and it would shock people because it’s true! I may even add it into this post if you’ll let me. Thanks for comment and for the share. Have a good week my friend?

No, new cars are nice. They are fun. Yes they do cost money. But life is short. Spend a bit and enjoy. Just stay within your budget.

Car payments truly do SUCK! 3 months ago we sold my beautiful 2013 Dodge Charger which came with a ~$500 month payment and we still have 3.5 years to go. We were able to walk away with ~$1,200 on the sale (that poor sucker who bought it from us can deal with the $500 a month payment now, sorry sir!), and we put in another $500 to buy ourselves a $1,700 1997 Toyota Avalon with 175k miles on it.

And you know what, I like that car just as much as I did my Charger. Every time I get in and it starts, I’m filled with joy about not spending a penny on that baby every month! Hopefully we can keep that car going for another 2 years and we should be at about 200k miles by then, sell it off for $500-$1000 and buy another ~$2k car to replace her.

Kyle,

Ha! I love it 🙂 You know what they call a 1997 Toyota Avalon that you pay $1,700 cash for? YOURS. I say this over and over again, but new cars lose 60% of their value in the first four years. This why we are always “upside down” in our cars and the payments keep coming each and every month. It ends up feeling like a way of life if you’re not careful. Good for you guys and send me a pic of your paid for 1997 Avalon over at my Facebook Page. Paid for cars look really good on it 🙂 Your reasoning for your purchse of the Avalon is exactly why we choose to Drive a Piece of Crap. Thanks for sharing Kyle.

We decided a long time ago that if we can’t pay cash for the car, we don’t need it.

I was recently reading a financial blog about people living above their means and the blogger said something like “Why can’t you make ends meet? Look under your feet and in your garage”.

Hi Steve!

I love that 🙂 “You don’t need to look too hard for why you are running out of money each month…it’s actually in your garage!” Now I wish I would have said that first! We also use the Cash in Full or we cannot afford it method. It sure has made life pretty simple too. Thanks for your comment Steve!

I agree car payments can suck, and when I was in school and needed a car, and didn’t have available cash, I found a great deal on a used car and had it paid off in ~2 yrs. When we went to get a “new” car for my wife we were set to just pay for it outright. Essentially get a loan, then transfer funds and pay it all off. Ultimately, we got a great trade in on her old car, and they got us 0% interest for the life of the loan. So we just invested the money we were going to use and have been making the payments instead. That’s a situation where it’s worth it to have payments and leave that chunk of $$ making more money for us.

Otherwise, I agree and say, car payments suck in SO many ways.

Hey Coffee Man! Thank you for the comment, but I am going to have to kindly disagree with you. Car payments suck all the time – even with 0% interest. The reason: 0% is never really 0%. Banks don’t loan out free money, which means they are still getting their money. When get “zero percent” you’re going to pay the interest somewhere else – usually by paying the extra the car is marked up to cover the “zero percent” interest. A buddy of mine is a manager at a car dealership and told me all of this. So, you’re always better to walk in w/ cash and pay $15k for a 17k car at zero percent interest.

Thanks for the comment and my reply was meant in all due respect – no jabs from me! ?

Available in more and more place, carsharing is fantastic alternative to the personally owned vehicle. If you can get to work some other way than driving, combining carsharing, cycling, walking, taxis, transit, and conventional rental car is almost always cheaper than owning a car and saves time and hassle too.

Kurt,

Great point! If you live in an area where carsharing is feasible, than by all means, do it (if it avoids a car payment). Thank-you my friend?

I sold my Mercedes Benz almost 5 years ago it has been the best financial decision I have ever made. I was paying over $300 month, not including an extra $300 in gas, maintenance, insurance, etc. Happy to be away from my MB!

Hey Even Steven! You were getting a deal at only $300/month for a Mercedes! I recently was working with someone paying $1,050/month for a Mercedes SUV on a lease! I would love to see your story from Mercedes to _______ in a blog post soon! Thanks for the comment!?

A Car is not a necessity… It is a luxury to own and operate and if you can’t afford one in cash then stop buying them.. In a couple of years time car prices will correct themselves and their cost will be affordable.. But common people never listen and don’t get it..

I am a share holder of more than a few car manufacturers so by all means by the most expensive cars and trucks you can and finance the SHIT out of them.. My brokerage and retirement accounts thank you.

Hey Tim! The number of people financing cars since 2009 has decreased, which is bad for your own retirement accounts and a positive for people trying to get out of debt and work towards financial freedom. I’m going to keep telling people to stay as far away from car loans as possible, but I still think you’re retirement accounts are safe?

They do! Just paid ours off yesterday. $16k in 9 months bitches.

Taking out a loan was the right and necessary decision for us but I’m glad to have it gone.

Hey hey hey!!! That’s awesome! Way to go? I would love to see a pic of that awesome car on the Money Peach Facebook Page! https://www.facebook.com/themoneypeach

Your timing is good. My 10 year old car (I bought it used for about 10k in 2008) is dying. Everything is breaking so I am going to sell it (any amount of money would be great) and just join the car share in my city. No hassles, no payments, no worries.

Nice Jo! Glad to hear that you’re not doing what 99.9999% of the world does when the car breaks or the check engine light comes on: “I’ll just go finance another for the next 67 months”. I would love to hear back from you on the Ride Sharing. Thanks Jo!

I wrote about my week with NO access to a car. It will get better.

https://deependofstupid.wordpress.com/2015/10/25/my-week-without-a-car/

I haven’t had a car payment in several years but it still hurts to think about it! Nice article and nice to see a lot of folks making smart choices.

Congrats Mr. Groovy! You’re bit normal for staying away from car payments. They’re a horrible way to spend money for the rest of your life. Thanks for the comment!

Rule #67 of Personal Finance: Don’t take budgeting advice from the dude selling you the car!

Wow, that really irritates the crap out of me. That’s not being a good salesman, that’s called being a creepy slime ball. Stay away from that dealership. Thanks for sharing and for the comment!

While most of my friends have brand new cars, I’m happy to drive my 2003 Honda CRV into the ground. There’s like a billion other things I’d rather do then have a car payment ever again!

It’s so sad that people assume a $200-$500+ car payment is just a way of life.

Nice post!

Thanks Vic! You’re 2003 is a lot like my 2002….finally starting to get all the kinks worked out 🙂 Thanks for the comment!

I had a 4 year old loan on my car. It cost about 12K Euro, I ended up paying almost double (fees, interest, premium insurance – something really really expensive, as I’d find out later). Its value now? Maybe 6K if I am lucky. The only upside to my stupidity is that we plan on using it till it ‘breaks’ and we did take great care of it anyway. It’s got about 40K miles on it, in perfect condition, even if almost 8 years old. I plan on using it at least 4-5 more years and then pay cash for a pre-owned car.

Hi Ramona!

Thanks for the comment. Your car has 40k miles on it? Congratulations, it’s officially now broken in 🙂 If you take care of this car and keep it for a while, then you’ll average out the depreciation and be in pretty good shape. Good luck!

I’m late to the party in commenting on this post… I am paying $320.00 a month on a 2010 Rav 4. I LOVE this car, I live in Vermont, I feel confident driving this car in the snow. I owe 11,000 on it. I can’t pay it off in 2 years, 3 seems more doable. I am a single parent and I work 20 miles from home with no available bus service. Toyota’s hold their value and I’m sure I could get a good price for it if I sold it, but I’m just not sure which direction to go here. I feel like I’d wind up paying for a lot of repairs if I bought an older “crap” car…where is the savings?? I’m actively working on a debt snowball, but I definitely live paycheck to paycheck. Should I include my car debt in my debt snowball?

Hi Marie!

Yes, you absolutely should include all debt except a mortgage inside your debt snowball. You also have a legitimate worry about dumping money into a “crappy used car”. I once thought the same thing, which is why we drove newer cars with car payments. Let’s break it down though:

You are paying $320/month for your car, or $3,840/year. If you bought a used car for $2k – $3k, would you really pay $3,840/year in repairs? Also, it gets worse…a newer car is going to have higher insurance costs, and higher registration fees. One more thing – an old “crappy” car is just about done losing it’s value, but your Rav 4 is still dropping (although the majority of it has depreciated by now). One more myth that I once believed true as well: cars holding their value. This is only true for less than 1% of the cars out there. The majority of cars such as yours are ALWAYS dropping in value. Always. Every. Single. Day. You know who tells people they are holding their value? Car Salesman. If I am in your shoes, I am selling the Rav 4 (even though I love it) and I am buying a piece of crap to drive for the next year. There is a slight possibility you will throw a little money at it for repairs….but remember, it’s a guarantee you’re going to shell out $3,840/year in payments. Sell the car 🙁

Thanks Chris…I’m looking at this totally differently now, honestly, I’ll be honest, a BIG part of my fear is being a single woman, in a broken down car!!! Going to give this some serious thought. Marie

Dude I love this post. I’m getting killed over here: we have 2 minivans we bought new to hold our growing family (we favor those giant space pod car seats that don’t fit in most cars). Problem is, we spend about $1k a month in car payments and I know we’re upside down on both of them (van 1 is 2y old has $25k left on it and van 2 is 2 months old and has $26k left on it) and we want to get out of this hell but how??? We don’t how to make the flow chart work for us.

Hi Derek!

Great question 🙂 Head over to Help! My Car is Upside Down and I’ll walk you step by step through the process.

Hey Chris. I look forward to reading your articles whenever I get a spare moment. I took your advice around the end of November and we started paying attention to our money flow. Our daughter is a freshman in high school and our son in sixth grade. I realized that I needed a plan that was going to free us up for when she goes to college and as he grows into driving/braces/glasses age. I sold my Jeep in December that I still owed 2 1/2 years on, was needing the occasional $300-$500 repair and paid it off. We took the difference and bought an older Honda (no payments), put $1k in our safe for unexpected emergencies, and began paying off our debts which included alot of medical and three credit cards. To date, we have paid almost $11,500 in debt off, with an extra $600/month to go toward debt. I took a second job and we are now putting around $1100/month to those debts. By Thanksgiving (one year after we started down this path) we will have paid off $18k in debt and given ourselves an $850/month raise. Then, our only debt should be our mortgage and a leased vehicle, which we will then either buy or get out of and get a different car we can pay off in under two years. We will then begin sinking funds for vacation and Christmas.

I don’t know if I’m more excited that our lives are about to change to that which we have always been jealous of or that we have done something very few people would be willing to do. It just gets better every day!

Hi Chris!

Right on brother! I am beyond excited for you can I’m sitting here thinking about how financial stable you’re going to be from here on out. Also, thanks for sharing your success! It’s not everyday you get to hear a story of someone taking extreme amounts of action and paying off $11k in only 4 months! Impressive 🙂 Life from here on out only gets better because not only will the stress of money go away, but like you said – money becomes exciting! Good job Chris! You’re doing big things and need to make sure to take a moment and give yourself a pat on the back. You’re a financial rockstar!

I kinda screwed up myself, but I’m not sure how I could have avoided it; I feel like a victim of circumstance.

So, I had bought a car and had it almost paid off, when it threw a rod and got ruined – was going to need a new motor. I needed a car, so I broke down and bought a 2010 Toyota Prius; since I put on about 40k business miles a year, not even counting personal miles, it seemed like a wise choice when taking into account gas prices. Meanwhile the other car sat there gathering dust with a ruined motor.

But then I got married, and my new wife and I needed a larger vehicle for when I had my kids, so we could all be in one car taking trips. So we traded in her car at a small used car dealership who was friends of my boss, and got a “good deal” on the suv. It was $2k under blue book.

Since then it’s become a money pit and we are doing repairs on it every month – sometimes twice a month! It’s driving us insane.

And now, with that debt, we are stuck, since its payoff is $19k, my prius is around the same, both are essentially under water here and getting their value would not be possible; I did manage to get my motor on my other car replaced, and tried to sell it at the low end of blue book value, and its in good shape now, but no one is nibbling, and this SUV’s constant repairs are eating us alive.

So now we are feeling trapped. Try and trade in the SUV to get a newer, more reliable car, and see our payments go up even higher? We really need at least a 6 seater for our larger family when my kids from my previous relationship are here, but the two cars aren’t going to sell for what we owe, and the third we can’t seem to sell despite it being in good shape.

And now we are looking to adding even more debt just to get out from under this money pit that’s eating us out of house and home. The real problem? I used to buy the older, used cars, and get them paid off quickly, but despite taking my best precautions, I’ve now had two cars that have had significant problems after purchasing them that have cost me far more than what they should have, thus making me very gunshy now about older used cars.

Not sure what to do. I really don’t want to add even more debt, but both cars HAVE to be reliable: I drive 40k miles a year just for work, and my kids live 4 hours away from me, I see them every other weekend, and drive a lot for that reason too. Because of those two reasons, I can’t have either car a POS that keeps breaking down and needing repairs, but lord, I am so tired of being in debt too.

Hi James,

Well, it looks like you got a lemon on your hands since you’re doing repairs on it once a month. This sounds like you got a bad deal from the “buddy” at the used car lot.

The bottom line is you need to get out from this money pit, and it’s not going to the easiest thing you’ve done, but you can do it – many people have and do this everyday.

Read this post to get an idea of where to start.

Get Out From Up Side Down Car

You can do this James 🙂

When I got out of college I bought a used car with payments. When the car was paid for I kept making those payments to a car savings account. When I needed a new car I had the money. I have done that for over 45 years. I kept my cars for 15+ years so Ihave always had money to pay cash for a new car when I needed one.

Linds,

You are the definition of the “Millionaire Next Door“. Great job and thanks for sharing. Can you imagine how much less your net worth would be if you spent 45 years making car payments to the bank?

Great job 🙂

Love this article. After I finished graduate school I was making great income and decided to “treat” myself by purchasing a brand new car with a nice hefty 675$ payment. Sooner or later along with other bills I got frustrated with the fact that I couldn’t grow my savings quickly and that I was basically living paycheck to paycheck even with a nice income. I got serious about budgeting and created a huge shovel to dump the car. I was so upside down with it being new I had to pay the heck out of it to get it to the even point so I could sell it. In addition to the payment I was paying an extra 2000$ a month on it. After paying it down about 14 to 15K dollars I finally sold it and even made a few bucks back on the sale. I went out a bought a fairly cheap 7K dollar little pick up truck cash and now I have no payment! Is a newer car or fancier car/truck nicer? Of course it is but driving a cheaper car doesn’t have to be forever. I plan to put away a certain amount now in a car fund so maybe next time I can buy a 10-12K car with cash and just keep building up that way. I’d say the best way to fend off the expensive car buying emotions is to refrain from comparisons to other people and just stay focused on one’s own goals and purpose.

My hubby and I are in a dark financial hole right now and the car payment is a huge part of that problem! We still owe nearly $12K! With everything else it will be a long while before we can tackle paying it off and I am clueless on how to go about selling it when you have a bank loan. Do you just try to sell for nearly the payoff amount or as much as you can and pay it towards the loan? What about buying something to replace it?

Hi Christina,

This is such a popular question on the blog which means you are not at all alone. I have a post that explains exactly what your options are and what you can do. Here is the link: Help! My Car is Upside Down. This will help guide you in the right direction 🙂

Hi Chris,

I know I am late to the discussion but what a great find! This is what my husband and I were just talking about this weekend. We need help! Guidence! A plan and fast! My husband put all our stuff on spreadsheets last week! We have two car payments totaling $850 a month and our credit card debit is $18k+ with $400 of the payment a month going to the interest only. We have student loan debit. But it’s the cars and credit cards that are killing us right now. We have no liquid cash left to really save because of these two. We bought our first house last year and our mortgage is lower then our rent was. Help!

Hi Shara, I think you’ll find the answers you need here on the blog and in my Awesome Money Course at AwesomeMoneyCourse.com. Let me know if you have other questions!